Let's Shape The Future Of Your Investments!

Natoque iaculis cursus augue urna commodo aptent morbi tortor porttitor quis ornare.

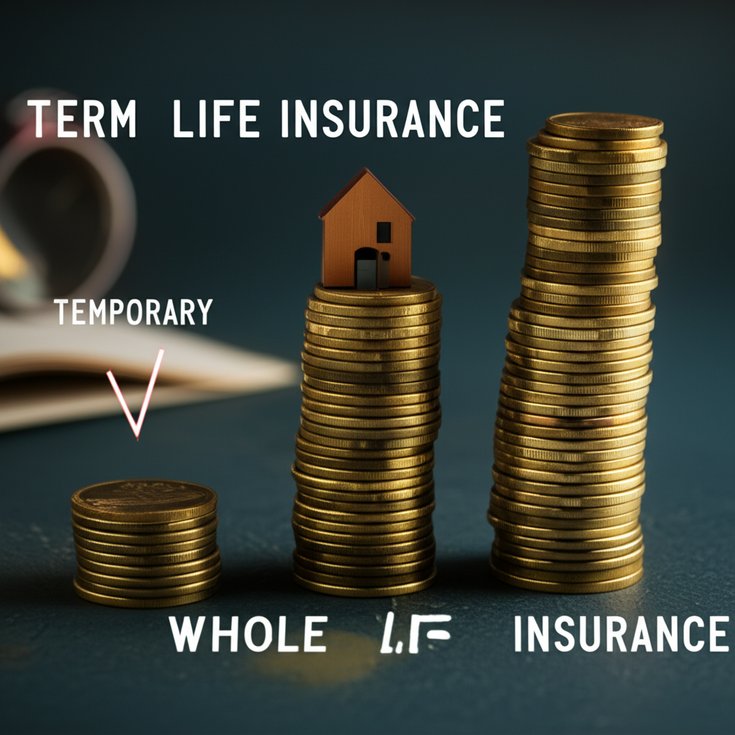

Choosing life insurance puzzles many people, especially when they ask, what is the difference between term and whole life insurance? Finding the right fit truly matters for family, business, and peace of mind.

If you keep reading, you will understand how each type of policy actually works. You will see real-life stories, cost breakdowns, and tips. I promise you will feel ready to talk about term vs whole life insurance with confidence.

Our team answers insurance questions every day, and we see how the structure of term and whole life insurance causes confusion. One grows value, one remains simple. Both can protect people well in the right situation.

When a person buys a term life policy, they agree to set coverage for a fixed period, often 10, 20, or 30 years. If you pass away during the term, your loved ones receive the death benefit. If you outlive the term, coverage stops.

People like term insurance for its lower starting cost. Many young parents choose it because they can get higher coverage when their kids need it most. There is no cash value in a regular term policy. The focus stays on providing financial protection rather than building savings.

Most families buy term life to cover mortgages, loans, or tuition bills. You pay steady premiums during the policy. You may ask, can I extend or convert it? In most plans, you can renew or even convert to whole life, but you must check your policy’s limits. If you need more advice, read our guide to understanding life insurance basics.

Whole life insurance covers a person from the day they start until death, no matter how long they live. Folks in our office often call it permanent life insurance, since it never runs out if you pay the premiums.

Whole life includes a savings part, known as cash value. This separate fund grows tax-deferred. As you pay premiums, a portion goes to this pool. Over years, it can grow a fair amount. You can borrow against it, or sometimes withdraw funds for emergencies.

Because whole life promises lifelong coverage and cash value, premiums start high and stay fixed. Families who want to create an inheritance grow fond of these policies. Unlike term, the benefit will always pay out, which gives peace of mind for covering final expenses or passing wealth.

Some people want large coverage for a short time, like mortgage years. Others want lifelong insurance plus savings. If you need quick, budget-friendly coverage, term suits you. If you value savings, want to pass money down, and keep coverage for life, whole life serves better. We always tell our clients: Matching policy features to personal needs leads to the right choice.

Term life insurance stands out because of its focus, simplicity, and upfront costs. Many people come to us unsure of the commitment, but term offers flexibility and minimal barriers to entry.

Buying term insurance feels straightforward. You choose a coverage period and an amount your family needs for financial security. Since the policy is pure death benefit, most companies approve policies fast—sometimes in the same week.

You just answer a few health questions and often do not need medical exams for lower coverage amounts. Policies rarely include extra benefits or cash value, which keeps the process clean and costs low. Our clients tell us they feel relief knowing what they pay buys protection, not complex extras.

When you compare life insurance cost, term comes out much lower than whole life, especially for young and healthy people. Premiums stay level for the selected term. Because there’s no cash value, you only pay for coverage. This appeals to people who want big coverage during high-responsibility years.

Let’s look at a basic cost comparison between a 30-year-old buying $500,000 coverage:

| Policy Type | Monthly Premium |

|---|---|

| Term Life (20 Years) | $25-$30 |

| Whole Life (Lifetime) | $300-$350 |

This shows the savings you get with term insurance. For some, this allows more money for daily needs or investments.

Many do not know you can often renew your term policy after it ends. But premiums increase with each renewal year as you age. Some companies let you change a term to whole life later, which helps if your financial needs change. You must act before your term expires.

Whole life insurance mixes protection and savings. People come to us curious about the cash value feature and how the cost stacks up over decades.

Each premium you pay into a whole life plan splits. A portion pays for your permanent coverage. Another part builds up cash value. In the early years, this savings part starts small but grows steady thanks to the insurer’s financial strength. Cash value earns interest and grows tax-deferred.

You can take out policy loans using this cash value. Some clients use these funds for emergencies, business needs, or even college bills. Policy loans lower the final death benefit if not repaid, but many families like the flexibility. At times, you can even withdraw part of your cash value, but this may change your coverage amount.

The insurance company guarantees the minimum interest rate you earn. For people worried about market swings, this gives a sense of safety. Regulations from bodies like the National Association of Insurance Commissioners add safety, making sure customer interests come first.

Whole life costs more for a good reason—it never expires. Your monthly payment stays fixed from day one. This means you avoid surprise increases in old age. For a healthy 35-year-old, the premium may seem high, but it never goes up. Our clients see value in knowing all costs, with no guessing about future increases like some term riders.

Because the policy pays out no matter when you pass, it helps families who want to leave money behind. Many use whole life for an inheritance or to meet legacy wishes. Others use it as part of business planning. People often find comfort knowing that, no matter when their time comes, their loved ones have crucial support.

If you value security and growth, see more about cash value life insurance policies for in-depth info. Our team guides clients through this decision daily, finding the right mix for return and protection.